2024 Hacash Outlook

A Review of the Top 10 Hacash Events of 2023 and Predictions for the Top 10 Trends of 2024.

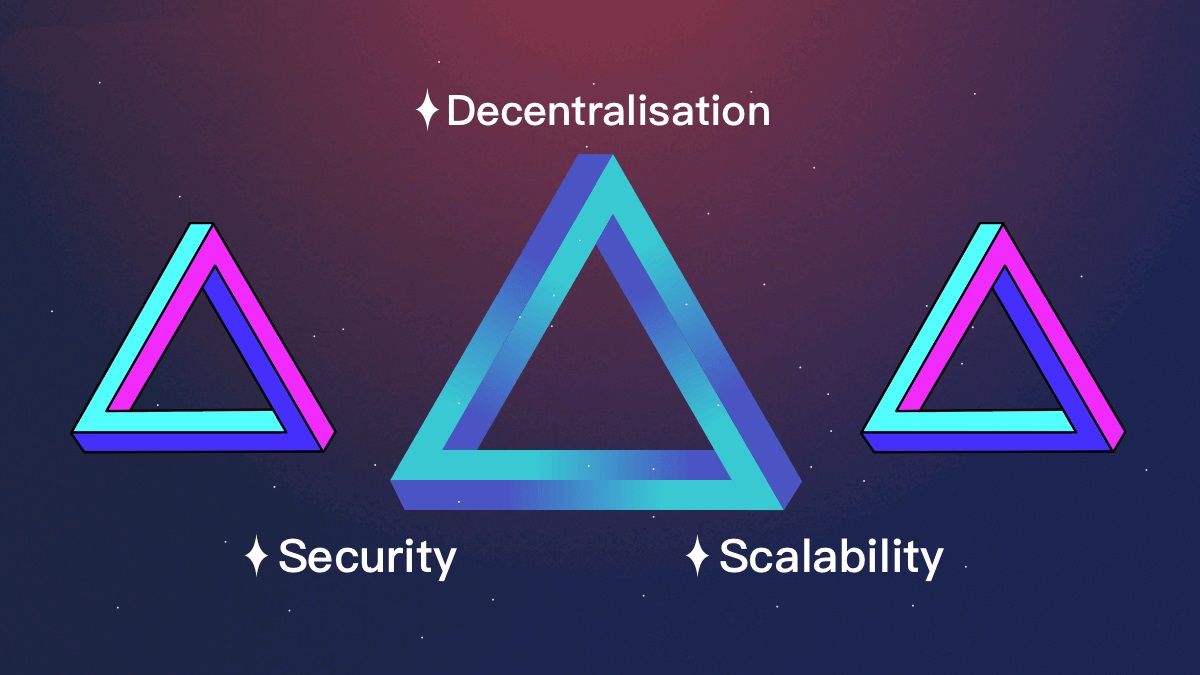

The article analyzes three impossible Trilemmas of the decentralized world as the core statement to examine Hacash's choices, to understand the underlying logic of Hacash, and see its overall vision clearly.

Co-Founder of HacashNews. Research Interests in Cryptocurrency & Money Theory.

© 2022 Hacash.com

All rights reserved.